Export Finance: Practical Lending Strategies Every Exporter Should Know

Brief Commentary on the TEXPROCIL Webinar | 8 July 2026

Attended by Salil Chawla, Director, DFU Publications

The Cotton Textiles Export Promotion Council (TEXPROCIL) organised an insightful webinar on 8 July 2026, bringing together exporters and industry stakeholders to discuss practical aspects of export finance and banking. Moderated by Dr. Siddhartha Rajagopal, the session provided a comprehensive overview of how banks evaluate exporters, structure working capital facilities, and manage risks associated with export credit.

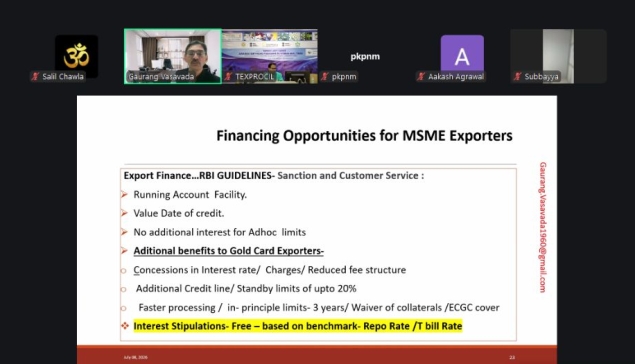

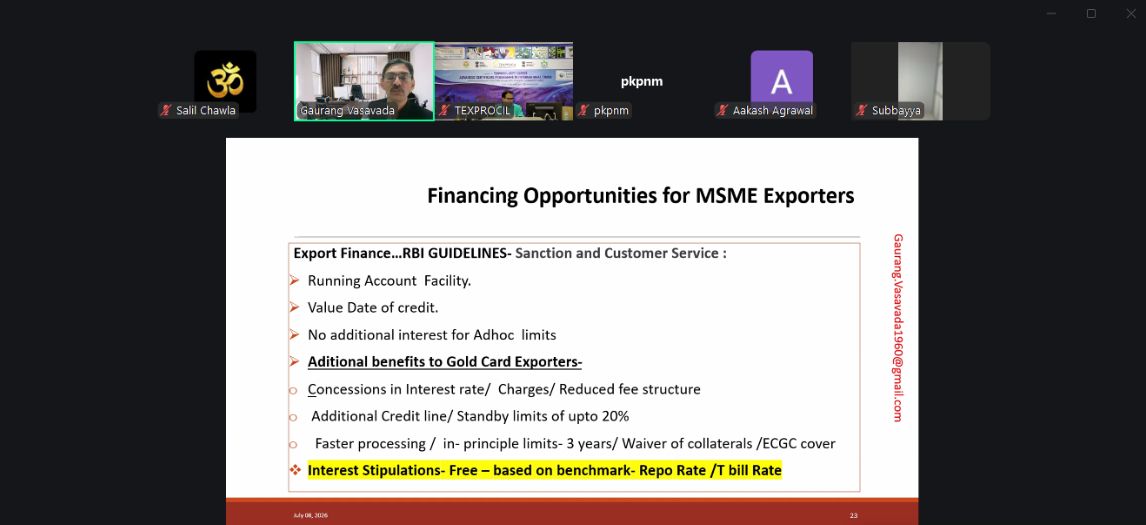

One of the key takeaways was that banks increasingly reward financially disciplined exporters. Businesses with a consistent repayment history and strong banking relationships may qualify for enhanced facilities such as Gold Card schemes, allowing them to access pre-approved standby credit limits without undergoing repeated sanction processes. Such flexibility significantly improves liquidity management for exporters.

The speaker explained that while banks have flexibility in determining lending rates, interest pricing must remain linked to recognised benchmark rates, such as the RBI's policy benchmarks for rupee loans. More importantly, banks assess every borrowing proposal based on five fundamental principles: Character, Capacity, Capital, Collateral, and Conditions. A strong repayment record, sound cash flows, adequate promoter contribution, reasonable security, and favourable industry and economic conditions collectively influence credit decisions.

Working capital assessment for exporters differs from conventional business lending. Since export cycles vary depending on buyer credit terms, banks generally prefer operating-cycle-based assessment rather than relying solely on turnover. Export inventory awaiting shipment forms the primary security, while additional collateral serves only as supplementary comfort to the lender.

The session also highlighted the important role played by Export Credit Guarantee Corporation (ECGC) guarantees in reducing lender risk. While guarantee schemes may cover a substantial portion of the credit exposure, banks continue to bear the balance risk, making prudent borrower evaluation essential. Diversification was another important recommendation, with banks encouraging exporters to avoid excessive dependence on a single overseas buyer or market.

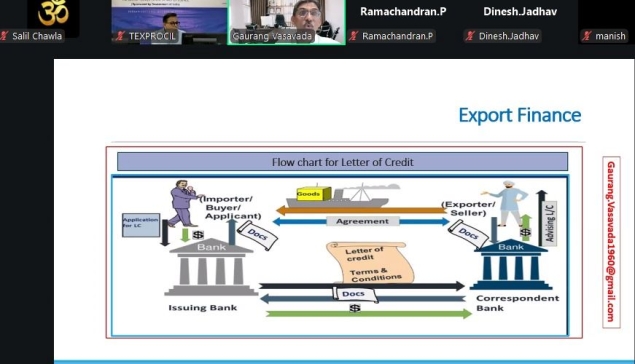

Through practical illustrations, the speaker demonstrated how a sanctioned working capital limit is typically divided among various facilities such as Cash Credit, Export Packing Credit (EPC), Post-Shipment Credit, Letters of Credit (LC), Bank Guarantees (BG), and Forward Contracts. Since these facilities draw from the same overall sanctioned exposure, utilisation under one component directly impacts the availability of others, making efficient cash-flow planning critical.

Another significant discussion focused on Export Packing Credit and post-shipment finance. Every export transaction is monitored individually through separate sub-accounts, each carrying its own shipment and repayment timeline. Delays in adjusting export bills can lead to penal interest, withdrawal of concessional export credit benefits, and eventual reclassification of the account if overdue periods exceed regulatory limits. Exporters were advised to proactively obtain buyer approvals for payment extensions and submit supporting documents to banks before the original due date.

An interesting cost optimisation strategy presented during the session compared commission-based trade finance structures with conventional interest-bearing facilities. Depending on the transaction period and financing arrangement, exporters may sometimes achieve lower financing costs through commission-based instruments such as Letters of Credit or buyer credit rather than relying solely on working capital borrowings.

The webinar also covered hybrid financing structures that combine collateral-backed lending with credit guarantee schemes, enabling exporters to access additional credit while optimising security requirements. Well-established exporters with strong banking relationships may also receive operational flexibility, including temporary packing credit against expected export orders, subject to timely submission of supporting documents.

Special attention was given to foreign currency export finance. The speaker explained that overseas currency borrowings are generally linked to international benchmark rates such as SOFR, offering potentially lower borrowing costs than domestic rupee finance. However, exporters must carefully manage foreign exchange exposure, as failed shipments or delayed export proceeds can result in conversion into higher-cost domestic liabilities.

The overarching message of the webinar was clear: effective export finance extends far beyond obtaining credit. Successful exporters actively manage documentation, shipment schedules, buyer communication, repayment timelines, and facility utilisation to minimise financing costs while preserving eligibility for concessional export credit. Strong banking discipline, timely compliance, prudent diversification, and strategic use of guarantee mechanisms remain essential pillars for sustainable export growth.